reset-roadmap

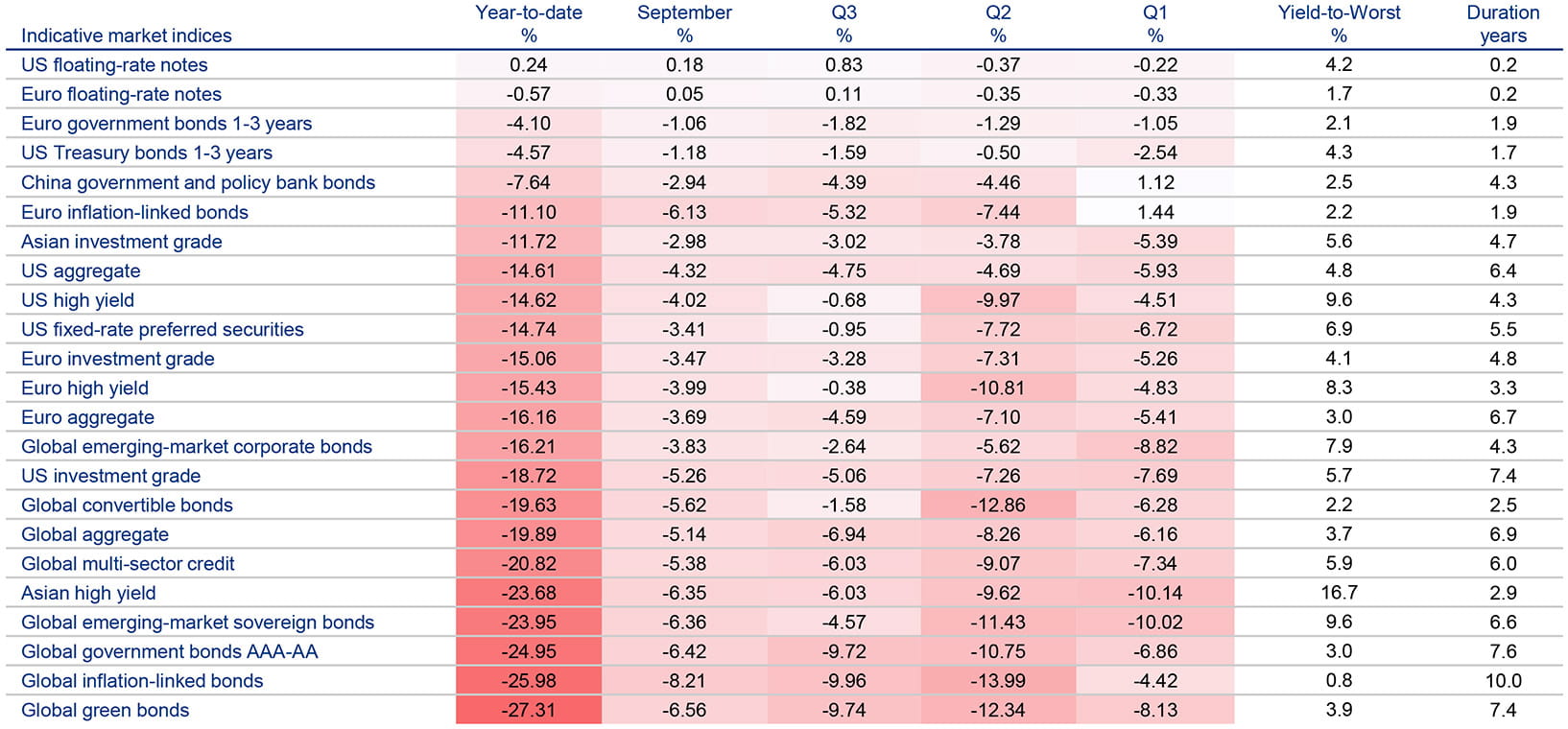

2022 will be remembered as a year of regime change in bond markets. Advanced economies entered a phase of higher inflation shocks not seen since the 1970s1 as policy and markets have become beholden to rising prices. Year-to-date, the number of public debt markets providing shelter for investors is close to

Exhibit 1: year-to-date, there have been few places for investors to hide in public debt markets

Source: Bloomberg. ICE BofA and JP Morgan indices; Allianz Global Investors. Data as at 30 September 2022. Index returns in USD (unhedged) except for Euro indices. Yield-to-worst adjusts down the yield-to-maturity for corporate bonds which can be “called away” (redeemed optionally at predetermined times before their maturity date). Effective duration also takes into account the effect of these “call options”. Past performance does not predict future returns. See the disclosure at the end of the document for the underlying index proxies. Investors cannot invest directly in an index. A rating provides no indicator of future performance and is not constant over time. Index returns are presented as net returns, which reflect both price performance and income from dividend payments, if any, but do not reflect fees, brokerage commissions or other expenses of investing.

Explore the four sections below for ideas for resetting bond allocations

Theme 1: a way to protect portfolios against market volatility

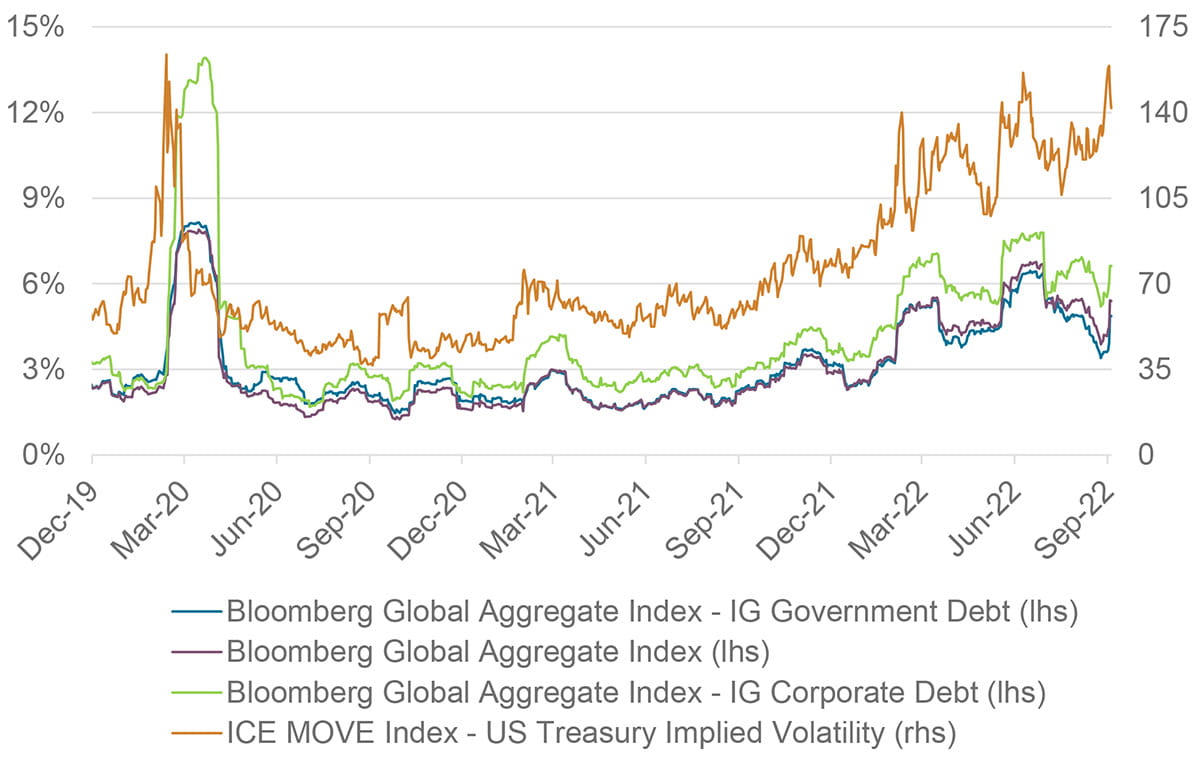

Realised and implied bond volatility are high and highly unstable

Measures of expected and realised bond volatility have come down from their recent peaks, but are still high.

Source: Bloomberg and ICE BofA indices. Allianz Global Investors. Data as at 30 September 2022. Index returns in USD (hedged). Realised volatility (30 days trailing) is annualised. IG= bonds rated Investment Grade. lhs=left-hand-side axis. rhs=right-hand-side axis. The rhs axis represents the value of the MOVE. which is a yield curve-weighted index of the normalised implied volatility on 1-month Treasury options on the 2. 5. 10 and 30-year contracts over the next 30 days. A higher MOVE value means higher option prices. Past performance does not predict future returns. See the disclosure at the end of the document for the underlying index proxies and important risk considerations. Investors cannot invest directly in an index. Index returns are presented as net returns, which reflect both price performance and income from dividend payments, if any, but do not reflect fees, brokerage commissions or other expenses of investing.

Where to Focus

- Strategies combining cash bonds with futures and options that help guard against rate and spread volatility could be considered. There can be associated cash outlay and performance costs.

- Floating-rate notes could help offer protection from rising rates. Keep in mind that floater yields tend to be lower than fixed-rate corporate bond yields.

Theme 2: navigating out-of-sync policies and economies

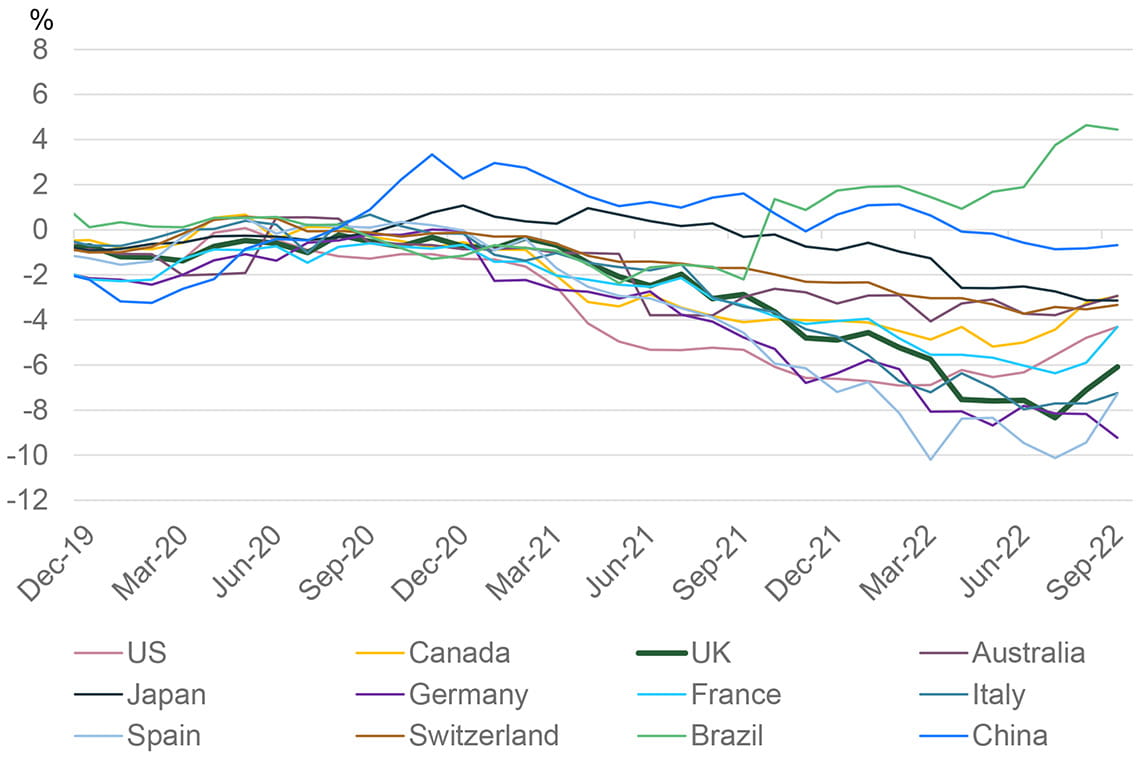

The divergence is feeding through to government bond markets

Local currency government bond yields adjusted for inflation suggest that economies and policies may be shifting in how and when they might exit the current inflation-led regime.

Source: Bloomberg. Allianz Global Investors. Yield data as at 30 September 2022. Latest available official inflation data for the month of August 2022. Month-end 1-year government bond yields (local currency) adjusted for monthly headline consumer price inflation (year-on-year, not seasonally adjusted). Past performance does not predict future returns.

Where to Focus

- The shift to an inflation-led regime may favour flexible bond strategies that could benefit from pricing discrepancies across global markets but also bring varying degrees of risks.

- It makes sense to consider allocating incrementally to those rates markets that could potentially benefit from flight to safety.

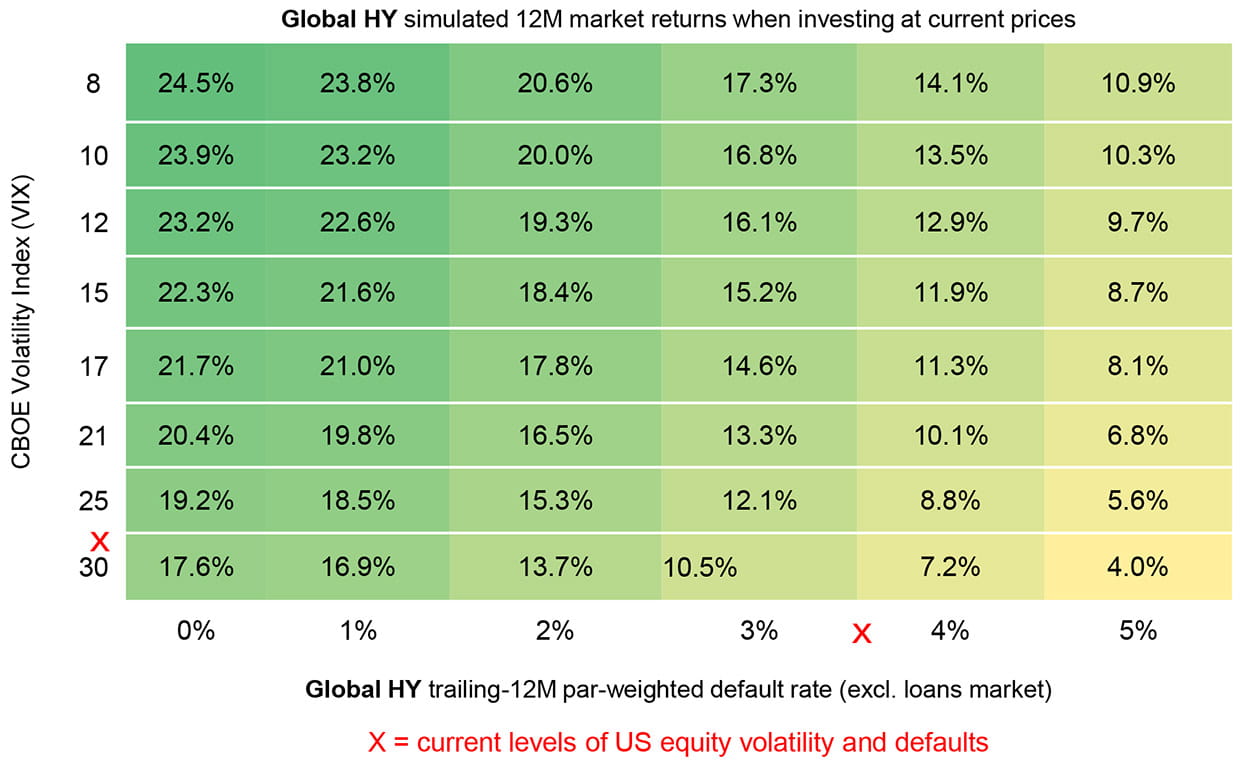

Source: Bloomberg. ICE. Allianz Global Investors. Data as at 30 September 2022. Global HY=ICE BofA Global High Yield Index. EM HC Sov=JP Morgan Emerging Market Bond Index (EMBI) Global Diversified. Past performance does not predict future returns. See the disclosure at the end of the document for the underlying index proxies, important risk considerations and simulation methodologies.

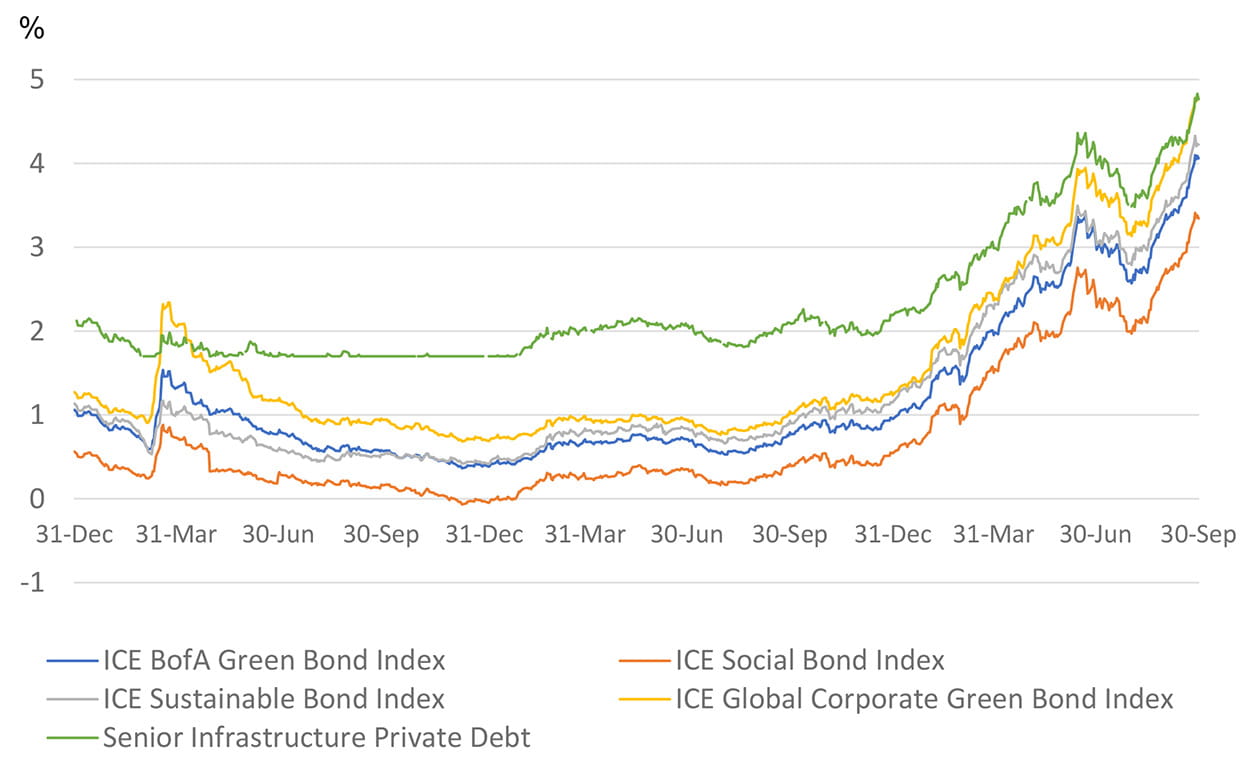

Source: Bloomberg, Allianz Global Investors. The yields for the ICE BofA indices represent the weighted average of the yields of the constituent bonds denominated in their local currency. The yield for investment-grade infrastructure private debt is an approximation, composed of the EUR 15-year mid-swap as a reference rate (with a floor at zero when it goes negative) + 170 basis points. Past performance does not predict future returns. See the disclosure at the end of the document for the underlying index proxies and important risk considerations. Investors cannot invest directly in an index.

Theme 3: a way to capture the value rebound in high-income assets

Once core rates and inflation stabilise, we believe high-income assets should follow soon afterAt current yields, high-yield corporates and emerging-market sovereigns could offer a good income cushion and upside.

Where to Focus

Theme 4: a way to benefit from the sustainable investing push

The energy crisis is boosting demand and yield for green and social financingYields offered by sustainability-labelled bonds have reset to more competitive levels.

Where to Focus